As spas around the world continue to embrace wellness, the more important physical activity is to their offering. By their very nature, spa-goers are interested in health. They come for a massage or facial to not only look good, but to feel good. Chances are they also keep fit in some way and they expect to see the latest workouts and innovations they’re accustomed to when they visit. It’s prudent, therefore, for spa operators to get an idea of the physical activity market – where it sits within the wellness arena, what the emerging trends are and what initiatives could encourage more people to move.

Size of the market

Cue a new study by The Global Wellness Institute (GWI). Move To Be Well: The Global Economy of Physical Activity was released at the Global Wellness Summit in Singapore in mid-October (see p82) and shows that the physical activity market is valued at US$828bn (€752bn, £655bn) and that it’s expected to reach US$1.1tn (€1tn, £870bn) by 2023.

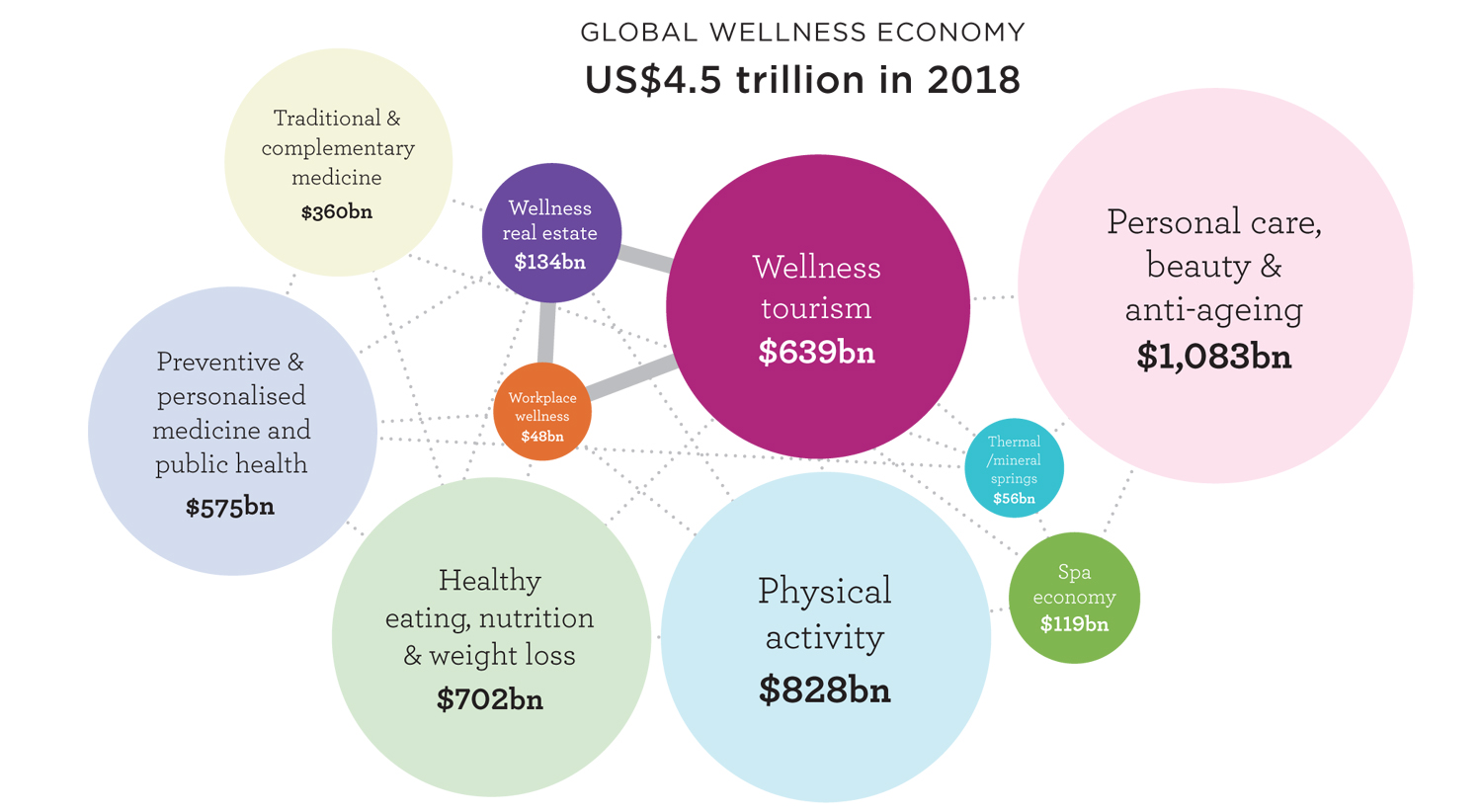

The market is made up of six sectors: sports and active recreation (US$230bn); fitness and gym (US$109bn); mindful movement (US$29bn); apparel/footwear (US$333bn); equipment/supplies (US$109bn); and fitness technology (US$26bn). Significantly, it’s the second largest market in the global wellness economy (see Diagram 1) which now jumps to US$4.5tn (€4.1tn, £3.5tn) in value with the new data.

Mindful movement

The mindful movement sector – which includes yoga, pilates, tai chi, qi gong, stretch, barre, Gyrotonic, etc – perhaps has the most affinity with spas. Of the world’s population, 3.8 per cent now regularly participates in mindful movement, spending US$101 a year on average.

Currently, it’s the second smallest sector in the physical activity market, yet given our frenetically-paced, stressful, sleepless and chronic-pain-plagued world, GWI expects mindful movement to skyrocket. In fact, it predicts it will become the fastest-growing sector, increasing 12.4 per cent annually and jumping from a US$29bn market in 2018 to US$52bn by 2023.

Breaking the sector down further, yoga is the biggest in terms of participants and value (165 million and US$16.6bn), followed by tai chi and qi gong (94.7 million and US$5.4bn) and pilates, barre and other modalities (28.9 million and US$6.7bn).

The US is by far the largest mindful movement market in terms of participation rate (17.7 per cent) and expenditures (US$10.4bn), followed by China (US$5.8bn), Japan (US$1.9bn), Russia (US$1.3bn) and Germany (US$1.2bn). Other countries with high participation rates include Australia, Canada, Denmark and New Zealand (all over 10 per cent). Although the sector is concentrated in wealthier countries at present, the report says “practices are spreading fast throughout the world”.

Fitness tech is another sector which spas can potentially tap into and should be paying attention to. Technologies make exercise more fun, affordable, personalised, portable, social, gamified and trackable and are experiencing an extraordinary uptake by consumers all over the world – even in countries that don’t have developed gym/fitness offerings. GWI marks this as the second-fastest-growing sector in the overall physical activity market and expects it to grow by 8.6 per cent a year to reach US$39.8bn by 2023.

Where in the world

Ninety per cent of the world’s spending on recreational physical activities takes place in North America, Asia and Europe (see Table 1). Globally, spending averages US$306 per participant per year: US$136 on activities and US$172 on equipment, apparel/footwear and technology. That number may seem low, but the study captures a broader range of physical activities than the US$200 a month elite gym membership or US$35 spinning class out of reach for most of the world.

In the future, the report predicts the physical activity economy will grow 6.6 per cent annually from 2018–2023, to surpass US$1.1tn. It says Asia-Pacific will overtake North America as the largest market, accounting for 40 per cent of all global growth. China and India together will drive nearly one-third of growth, while the US will account for one-quarter.

Market size and the highest rates of recreational physical activity participation don’t often correlate, and the report looks at what percentage of the population of 150 nations regularly take part in sports and active recreation, fitness or mindful movement. Australia and Taiwan lead the world with 84 per cent recreational physical activity participation rates. Interestingly, when you compare the happiest nations from the 2019 World Happiness Report to the countries with the highest rates for recreational physical activity, there’s very striking overlap. Fourteen nations make both top 20 lists, with Nordic countries such as Norway, Iceland, Sweden, Finland and Denmark all ranking in the top 10 for “happiest” and most physically active. The movement and “mood” connection seems powerful.

Mind the gap

Despite the ever-increasing consumer spending on physical activity, the report highlights that expenditure is “not necessarily the solution to the global crisis of physical inactivity” and that up to two-thirds of adults lead sedentary lifestyles according to the World Health Organization.

From a public health perspective, the aim is simply to get more people more active, more often – regardless of whether they spend more money while doing so. Yes innovations – from apps and US$100 fitness bands to a US$2,500 high-tech treadmill – can enhance the exercise experience, but they also remain out of reach for large swaths of the world’s population.

In fact, we do not have to spend any money at all in order to be physically active and stay healthy, especially when we have access to good parks, recreation, and outdoor amenities, and when we get enough “natural movement” in our daily lives. Government investment in public infrastructure, parks, outdoor gyms, school programmes and physical education, is critically important in this respect. But GWI firmly believes that both the public and private sectors – including spas and fitness centres – must work together to address the physical inactivity crisis.

The solution lies in addressing the major barriers to physical activity and GWI reviewed over 75 studies and surveys across 60 countries to identify the problem areas. Among adults, the top reasons for not engaging in physical activities are: lack of time; lack of interest; physical or health conditions; and lack of motivation or habit. Among younger people, the main reasons are: lack of time; lack of convenient facility or activity near home; not having fun; and prefer to do something else.

The full 180-page report provides numerous examples of innovations, new business models, and public policy initiatives that can help overcome barriers to physical activity, increase participation, and extend the many benefits of movement to more people around the world. Some of the approaches most relevant to spas are summarised below:

Mitigating time constraints and increasing convenience by using apps and digital services to enable workouts on demand; or via the fitness-hospitality nexus which makes it easier for people to exercise when travelling.

Making physical activity a daily habit by offering workplace wellness initiatives which incorporate physical activity into work days.

Making physical activity fun and appealing by introducing things like ‘dance as exercise’; by incorporating technology to make fitness enjoyable and rewarding; or by building connections with leaders, teams, tribes, and communities.

Enabling movement in all physical conditions. Most businesses today serve people who are already active or capable of conducting physical activity, excluding those who find it difficult to participate such as people with physical conditions related to age, medical conditions, disability, injury, etc. There are opportunities to serve this population from mainstreaming therapeutic and recovery fitness to tapping into the grey market or working on exercise as a prescription.

Embedding physical activity in the built environment – take a look at the wellness real-estate model for example.

Making physical activity affordable and accessible to everyone by introducing high-value, low price fitness options; by making spaces safe and comfortable for women; and by recognising the importance of small businesses in serving communities.

In summing up the findings of the research, GWI senior researcher and report co-author Ophelia Yeung says: “This new global data stream is meant to encourage business leaders and policy makers to see physical activity as a comprehensive sector, and one that’s critical in supporting lifestyles that are crucial to good health.

“Yes, physical activity has become a massive US$828bn commercial segment, but the conundrum is that sedentary lives, obesity and chronic disease are all exploding right alongside it.”

Katherine Johnston, also a GWI senior researcher and co-author, concludes: “When people think ‘fitness industry’ they think gyms, boutique studios, yoga and fit-tech like wearables, but there are so many ways we can exercise to stay healthy – from playing sports to dancing to biking to work. And there are huge opportunities for businesses to get more people active – beyond affluent urbanites/suburbanites, the young and the already-healthy.”