One thing's certain in life and business, and that's change. Fortunately, when it comes to the industry, change often equals growth. According to the IHRSA Global Report: The State of the Health Club Industry, revenues in 2015 totalled US$81bn, from 151 million people visiting 187,000 clubs.

Just a year later, in 2016, those numbers jumped to US$83.1bn in revenue, 201,000 clubs, and 162.1 million members.

Last year the word ‘stability’ was used to describe the Global 25 list of the most successful and respected companies in the industry. This year, some new names have appeared at the top of several categories.

SITE NUMBERS

In terms of number of facilities owned, the 2016 list is topped by the same four companies as in 2015: LA Fitness International, LLC; 24 Hour Fitness USA, Inc.; Basic-Fit/HealthCity; and GoodLife Fitness and Énergie Cardio. However, Bio Ritmo has moved up several places, from eighth to fifth; McFit has retained its 7th place position; and ClubCorp has risen from 10th to eighth place.

The companies dominating the industry, in terms of membership numbers, have shown some change since 2015. Some of the top seven companies have gained members, some lost members and others have stayed the same. Top of the list for 2016 is Planet Fitness, with 8.9 million members, up from 7.3 million. In second place is 24 Hour Fitness USA, Inc., with 3.8 million, unchanged. Gold’s Gym International places third with 3 million, unchanged, and Anytime Fitness is fourth, with 2.85 million, up from 2.6 million. Fifth place belongs to McFit, with 1.4 million, up from about 1.37 million. GoodLife Fitness and Énergie Cardio are both sixth on the list, with 1.3 million, up from 1.26 million. Finally, Powerhouse Gym is at seventh place, with 1.2 million.

Looking back to 2015, the first five rankings are identical. However, GoodLife Fitness and Énergie Cardio have moved up from seventh place to sixth this year, and Bio Ritmo/Smart Fit has moved up one notch, from ninth position to eighth in 2016.

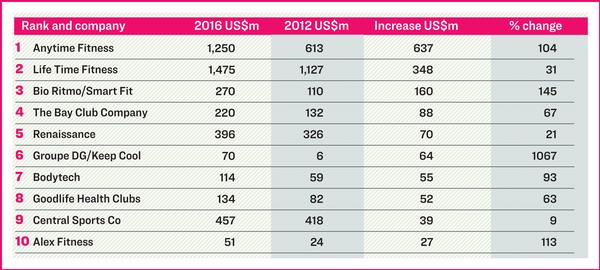

REVENUE RANKINGS

For 2016, the top seven chains were: Planet Fitness (US$1.9bn); Life Time Fitness, (US$1.475bn); Anytime Fitness, (US$1.25bn); ClubCorp ($1.088bn); Fizek Fitness (US$587m); Snap Fitness (US$563m); and Central Sports (US$457m).

In comparison, the top seven in 2015 were: Planet Fitness (US$1.5bn); Anytime Fitness (US$1.1bn); ClubCorp (US$1.05bn); Fitness First Finance, Ltd. (US$677m); Snap Fitness (US$555m); and David Lloyd Leisure (US$510m). This shows franchised operations are beating company-owned clubs in the revenue category.

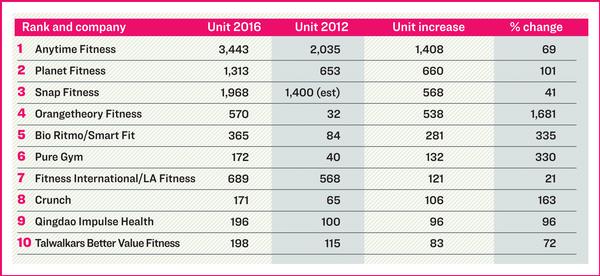

Franchise figure rankings for 2016 have also showed change. For 2016, numbers one through three are the same as in 2015. They are: Anytime Fitness (up 388, to a total of 3,443 units); Snap Fitness (up 521 to 1,968); and Planet Fitness (up 192, to 1,313).

Mrs.Sporty has gained 27 units to make a total of 578, placing the company in fourth place, up from fifth in 2016.

Orangetheory Fitness, which has added an impressive 245 stores since 2015, is now fifth on the list, with 570. Gold’s Gym International has dropped from fourth place in 2015, to sixth in 2016, after maintaining its 700-plus locations. Finally, 9Round is seventh on the list with 497 sites, up from 456.

There is no question that the experience of change can be challenging. But most would agree that change is a good, or rather, a great thing when it leads to consistent growth – based on strong business models that consumers want here and now, and ones that are predicated on well-executed strategic plans.

The leading fitness companies on the IHRSA Global 25 list are proof of the truth of that today, and are likely to remain so in 2017, as well.